Your home is likely your biggest investment, and protecting it with the right insurance isn’t optional—it’s essential. In 2026, American homeowners are paying an average of $2,377 annually for home insurance, but rates vary dramatically based on location, home characteristics, and coverage choices. Understanding what drives these costs and how to reduce them can save you $800 to $1,500 per year while ensuring your most valuable asset stays protected.

What Is Home Insurance and Why Do You Need It?

Home insurance (also called homeowners insurance) is a property insurance policy that covers your home’s structure, personal belongings, and liability for injuries or damage that occur on your property. If you have a mortgage, your lender requires home insurance to protect their investment. Even if you own your home outright, going without coverage is a massive financial risk.

According to the Insurance Information Institute, the average home insurance claim is $13,759, with major disasters like fires averaging $79,000 in damages. Without insurance, these costs come directly from your savings—potentially devastating your financial security.

How Much Does Home Insurance Cost in 2026?

National Average Rates

The average annual home insurance premium in the United States for 2026 is $2,377, which breaks down to approximately $198 per month. However, this varies significantly:

- Least expensive: Around $900-$1,200 annually (states like Vermont, Wisconsin)

- Most expensive: $4,000-$11,000 annually (states like Florida, Louisiana)

Home Insurance Cost by State (2026)

| State | Average Annual Premium | % Above/Below National Average |

|---|---|---|

| Florida | $10,996 | +363% |

| Louisiana | $6,354 | +167% |

| Texas | $4,456 | +87% |

| Oklahoma | $4,128 | +74% |

| Kansas | $3,897 | +64% |

| Colorado | $3,654 | +54% |

| Nebraska | $3,521 | +48% |

| California | $2,115 | -11% |

| Oregon | $1,356 | -43% |

| Idaho | $1,287 | -46% |

| Utah | $1,245 | -48% |

| Vermont | $1,054 | -56% |

Note: Florida’s rates have increased dramatically due to hurricane risk, litigation costs, and insurance company insolvencies.

Why Such Dramatic Differences?

Climate and Natural Disaster Risk States prone to hurricanes, tornadoes, wildfires, or earthquakes face significantly higher premiums:

- Hurricane zones (FL, LA, TX): 150-350% above average

- Tornado Alley (OK, KS, NE): 50-75% above average

- Wildfire regions (CA, CO): 20-50% above average

- Earthquake zones: Require separate coverage

Construction Costs Areas with higher labor and material costs see elevated premiums:

- Major metropolitan areas: 15-25% higher

- Remote locations: 10-20% higher (limited contractor availability)

Crime Rates High-theft areas face increased premiums for theft coverage:

- Urban centers: 5-15% higher

- Low-crime suburban areas: 5-10% lower

Litigation Environment States with frequent insurance lawsuits see higher rates:

- Florida’s litigious environment adds $1,000-$1,500 to average premiums

What Does Home Insurance Cover?

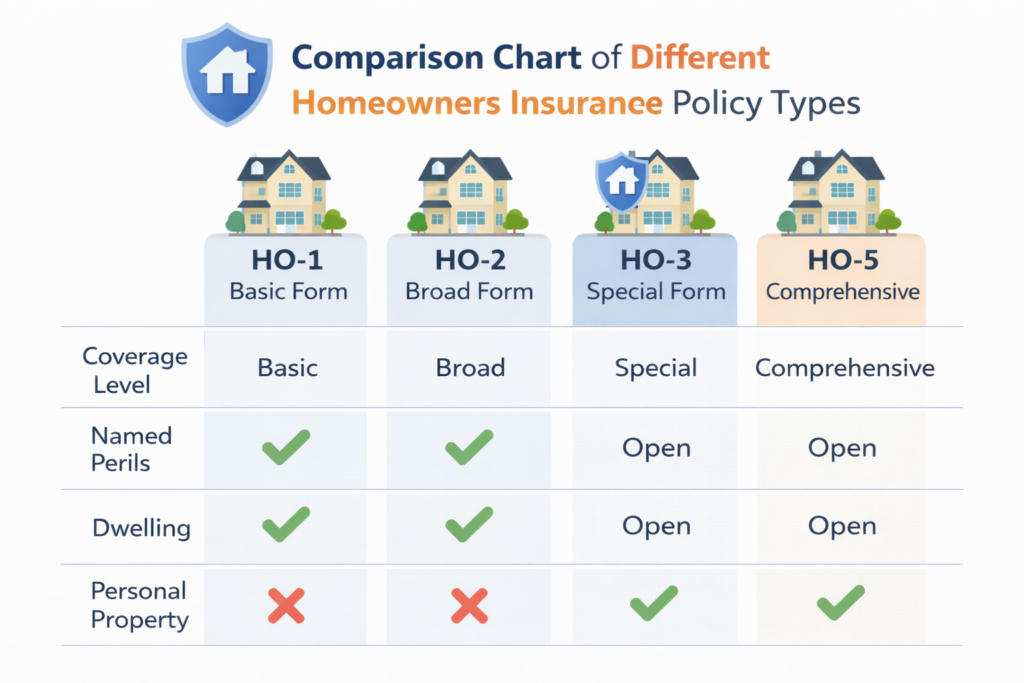

Standard Homeowners Policy (HO-3)

The most common policy type, HO-3, provides “open peril” coverage for your dwelling and “named peril” coverage for personal property.

Dwelling Coverage (Coverage A) Protects your home’s structure, including:

- Walls, roof, and foundation

- Built-in appliances

- Attached structures (garage, deck)

- Plumbing, electrical, and HVAC systems

Recommended coverage: 100% replacement cost of your home (not market value)

Other Structures (Coverage B) Covers detached structures:

- Separate garage or shed

- Fences and gates

- Pool house or gazebo

Typical limit: 10-20% of dwelling coverage

Personal Property (Coverage C) Protects your belongings:

- Furniture and appliances

- Clothing and electronics

- Jewelry (with sub-limits)

- Sports equipment

Typical limit: 50-70% of dwelling coverage

Important: Standard policies have sub-limits on high-value items:

- Jewelry: $1,500-$2,500

- Collectibles: $2,500-$5,000

- Cash: $200-$500

- Electronics: $2,500-$5,000

Consider scheduled personal property endorsements for valuable items.

Loss of Use (Coverage D) Pays for temporary living expenses if your home is uninhabitable:

- Hotel or rental costs

- Restaurant meals (above normal food costs)

- Storage fees

- Pet boarding

Typical limit: 20-30% of dwelling coverage for 12-24 months

Personal Liability (Coverage E) Protects you if someone is injured on your property or you damage their property:

- Medical expenses for injured guests

- Legal defense costs

- Settlements and judgments

Standard limit: $100,000-$300,000 (Experts recommend at least $300,000-$500,000)

Medical Payments (Coverage F) Covers minor medical expenses for injured guests regardless of fault:

Typical limit: $1,000-$5,000

What’s NOT Covered by Standard Policies

Common Exclusions:

- Flood damage: Requires separate NFIP or private flood insurance

- Earthquake damage: Requires separate endorsement (except in California, where it must be offered)

- Sewer backup: Often excluded, add endorsement for $40-75/year

- Mold: Limited coverage unless caused by covered peril

- Wear and tear: Maintenance issues aren’t covered

- Business property: Need business insurance for home-based businesses

- Certain dog breeds: Some insurers exclude breeds considered high-risk

- Intentional damage: Self-inflicted or purposeful damage

- Neglect: Damage from lack of maintenance

Water Damage Complexities:

- Covered: Sudden pipe burst, appliance malfunction

- Not covered: Gradual leaks, poor maintenance, groundwater seepage

Types of Home Insurance Policies

| Policy Type | Best For | Coverage Highlights | Average Cost |

|---|---|---|---|

| HO-1 (Basic) | Minimal coverage needs | 10 named perils only | $800-$1,200 |

| HO-2 (Broad) | Budget-conscious owners | 16 named perils | $1,200-$1,800 |

| HO-3 (Special) | Most homeowners | Open peril dwelling, named peril contents | $1,800-$2,600 |

| HO-4 (Renters) | Renters | Personal property and liability | $180-$350 |

| HO-5 (Premier) | High-value homes | Open peril for dwelling AND contents | $2,500-$4,000 |

| HO-6 (Condo) | Condo owners | Interior and personal property | $400-$900 |

| HO-7 (Mobile) | Mobile homes | Mobile home-specific coverage | $800-$1,500 |

| HO-8 (Older Homes) | Historic homes | Actual cash value, not replacement | $1,000-$1,800 |

HO-3 vs. HO-5: Is Premium Coverage Worth It?

HO-5 costs 20-40% more but offers:

- Open peril personal property (broader coverage)

- Higher limits on valuables

- Guaranteed replacement cost (even if costs exceed policy limits)

- Better coverage for electronics and jewelry

Worth it if: You own high-value items, prefer comprehensive protection, or live in areas with unique risks.

Factors That Affect Your Home Insurance Cost

Home Characteristics

1. Age of Home

- New homes (0-10 years): 10-20% lower premiums

- Older homes (50+ years): 15-30% higher premiums

- Historic homes (100+ years): May require specialized coverage

Why: Newer homes have updated electrical, plumbing, and roofing, reducing claim likelihood.

2. Construction Materials

- Brick/stone: 5-15% lower (fire-resistant)

- Wood frame: Standard rates

- Stucco: 5-10% lower in some regions

- Log homes: 10-25% higher (fire risk)

3. Square Footage Larger homes cost more to insure:

- 1,000-1,500 sq ft: $1,200-$1,800

- 2,000-2,500 sq ft: $1,800-$2,400

- 3,000-3,500 sq ft: $2,400-$3,200

- 4,000+ sq ft: $3,200-$5,000+

4. Roof Condition and Type

- New roof (0-5 years): 10-15% discount

- Older roof (15+ years): 10-25% surcharge or coverage denial

- Impact-resistant shingles: 5-10% discount

- Metal roofing: 10-15% discount (longevity, fire resistance)

5. Home Features Increase premiums:

- Swimming pool: $25-75/year

- Trampoline: $50-100/year or coverage denial

- Wood-burning stove: 5-10% surcharge

- Hot tub: $25-50/year

Decrease premiums:

- Security system: 5-20% discount

- Fire sprinklers: 5-15% discount

- Smart home devices: 5-10% discount

- Gated community: 2-5% discount

Personal Factors

Credit Score Impact In states where permitted, credit-based insurance scores affect rates:

- Excellent credit (750+): Baseline or 5% discount

- Good credit (700-749): Standard rates

- Fair credit (650-699): 10-20% higher

- Poor credit (below 650): 25-50% higher

States prohibiting credit-based scoring: California, Maryland, Massachusetts, and Hawaii

Claims History

- No claims (5 years): 15-25% discount

- One claim (3 years): 10-20% increase

- Two claims (5 years): 25-40% increase

- Three+ claims: May face non-renewal

Deductible Selection Your deductible dramatically affects premiums:

| Deductible | Annual Premium | Savings vs. $500 |

|---|---|---|

| $500 | $2,400 | Baseline |

| $1,000 | $2,040 | 15% ($360/year) |

| $2,500 | $1,680 | 30% ($720/year) |

| $5,000 | $1,440 | 40% ($960/year) |

Choose higher deductibles only if you can afford the out-of-pocket expense.

Top Home Insurance Companies in 2026

Best Overall Providers

1. Amica Mutual

- Average annual cost: $2,156

- Customer satisfaction: 4.8/5

- Best for: Excellent customer service, comprehensive coverage

- Unique feature: Disappearing deductible (reduces $100/year claim-free)

2. USAA

- Average annual cost: $1,945

- Customer satisfaction: 4.9/5

- Best for: Military members and families

- Unique feature: Valuables coverage without separate endorsements

3. State Farm

- Average annual cost: $2,239

- Customer satisfaction: 4.5/5

- Best for: Local agent support, bundling

- Unique feature: Extensive agent network (19,000+ agents)

4. Chubb

- Average annual cost: $3,800+

- Customer satisfaction: 4.7/5

- Best for: High-value homes, premium coverage

- Unique feature: Agreed value coverage, no depreciation

5. Nationwide

- Average annual cost: $2,187

- Customer satisfaction: 4.3/5

- Best for: Brand new belongings coverage

- Unique feature: Better Roof Replacement (full replacement cost)

6. Allstate

- Average annual cost: $2,450

- Customer satisfaction: 4.2/5

- Best for: Claim forgiveness programs

- Unique feature: Claim-Free Bonus (refunds deductible after 6 claim-free years)

7. Liberty Mutual

- Average annual cost: $2,398

- Customer satisfaction: 4.1/5

- Best for: Customization options

- Unique feature: New home discounts up to 20%

8. Farmers

- Average annual cost: $2,512

- Customer satisfaction: 4.2/5

- Best for: Flexible coverage options

- Unique feature: EcoRebuild coverage for green rebuilding

Best Budget Options

- Lemonade: $1,200-$1,800 (AI-powered, fast claims, newer homes)

- Hippo: $1,400-$2,000 (Smart home integration, home maintenance perks)

- Kin: $1,300-$1,900 (Florida specialist, competitive hurricane coverage)

How to Save Money on Home Insurance

Immediate Discounts You Can Request

1. Bundle/Multi-Policy Discount: 15-25% savings Combine home and auto insurance with the same company:

- Average savings: $300-$600/year

- Works with renters, umbrella, and life insurance too

2. Security System Discount: 5-20% savings Install monitored security systems:

- Basic alarm: 5-10% discount

- Monitored system: 10-15% discount

- Smart home security: 15-20% discount

3. Fire Protection Discount: 5-15% savings

- Smoke detectors: 2-5% (often required)

- Fire extinguishers: 2-3%

- Sprinkler system: 5-15%

- Fire-resistant roofing: 5-10%

4. Storm Protection: 5-20% savings Especially valuable in hurricane/tornado zones:

- Hurricane shutters: 5-15%

- Impact-resistant windows: 10-15%

- Reinforced garage door: 3-5%

- Safe room: 5-10%

5. Claims-Free Discount: 10-25% savings Maintain a clean record:

- 3 years claim-free: 10-15%

- 5 years claim-free: 15-20%

- 10 years claim-free: 20-25%

6. New Home Discount: 10-20% savings Homes less than 10 years old qualify.

7. Gated Community/Secure Location: 2-7% savings Reduced theft risk translates to lower premiums.

8. Loyalty Discount: 5-10% savings Staying with the same insurer:

- 3 years: 5%

- 5 years: 7%

- 10+ years: 10%

But don’t let loyalty prevent comparison shopping—you might save more by switching.

9. Automatic Payment/Paperless: 3-5% savings Enroll in autopay and electronic documents.

10. Professional Association: 5-10% savings Many employers, alumni associations, and professional groups offer insurance discounts.

Strategic Ways to Reduce Costs

Increase Your Deductible Moving from $500 to $1,000 deductible saves 15-20% annually:

- Only do this if you have emergency savings

- Avoid filing small claims (save insurance for major losses)

Improve Your Credit Score In states where credit affects rates, improving from fair to good credit can save $200-$400/year.

Review and Adjust Coverage Annually

- Remove coverage for items you no longer own

- Adjust dwelling coverage if you’ve paid down mortgage significantly

- Ensure you’re not over-insured on depreciated belongings

Don’t File Small Claims Filing claims under $2,500-$5,000 often costs more long-term:

- Rate increase: 10-20% for 3-5 years

- Potential non-renewal

- Save insurance for catastrophic losses

Shop Around Every 2-3 Years Rates change frequently:

- Get quotes from 3-5 companies

- Use independent agents who represent multiple insurers

- Leverage competitive quotes to negotiate with current insurer

Ask About Lesser-Known Discounts

- Non-smoker discount: 2-5%

- Renovated home: 5-10% for major updates

- Water shutoff device: 3-5%

- Roof age certification: 5-10% for new roof documentation

Read Also: Commercial Property Insurance in the USA (2026): Cost, Coverage & Best Policies for Small Businesses

Common Home Insurance Mistakes to Avoid

1. Underinsuring Your Home

40% of homes are underinsured by 20-50%, according to insurance industry estimates. This happens when:

- Insuring for market value instead of replacement cost

- Not accounting for inflation and construction cost increases

- Failing to update coverage after renovations

Solution: Get a professional replacement cost estimate every 3-5 years. Ensure your policy includes:

- Inflation guard: Automatically increases coverage (usually 2-4% annually)

- Extended replacement cost: Covers 125-150% of dwelling limit if costs exceed estimate

2. Not Understanding Replacement Cost vs. Actual Cash Value

Replacement Cost Coverage

- Pays to rebuild/replace without depreciation

- Higher premiums (10-15% more)

- Best for most homeowners

Actual Cash Value Coverage

- Pays depreciated value

- Lower premiums

- Suitable only for older homes you plan to demolish

Example: 10-year-old roof damaged in storm

- Replacement cost: Pays $15,000 for new roof

- Actual cash value: Pays $7,500 (50% depreciation)

3. Neglecting Additional Coverage for Valuables

Standard policies have low sub-limits on valuable items:

- Jewelry: $1,500-$2,500 total

- Collectibles: $2,500-$5,000

- Electronics: $2,500-$5,000

Solution: Purchase scheduled personal property endorsements (floaters):

- Cost: $1-$2 per $100 of coverage

- Covers all perils including accidental loss

- No deductible applies

- Example: $10,000 engagement ring = $100-$200/year

4. Ignoring Flood and Earthquake Coverage

These are ALWAYS excluded from standard policies:

Flood Insurance

- Required if in high-risk flood zone with mortgage

- Available through NFIP or private insurers

- Average cost: $700-$1,500/year

- Covers dwelling and contents separately

Earthquake Insurance

- Average cost: $800-$3,000/year (varies dramatically by location)

- High deductibles (10-25% of dwelling coverage)

- Essential in California, Pacific Northwest, New Madrid Seismic Zone

5. Not Documenting Your Belongings

Without proof, claims are difficult:

- Create video/photo inventory of all rooms

- Keep receipts for high-value purchases

- Store documentation off-site (cloud storage, safe deposit box)

- Update annually

Helpful apps: Sortly, Nest Egg, Encircle

6. Choosing the Wrong Deductible

Too low: Overpaying on premiums for minor savings protection Too high: Can’t afford out-of-pocket expense when disaster strikes

Rule of thumb: Choose a deductible you can comfortably pay from emergency savings.

Filing a Home Insurance Claim: What to Expect

Step-by-Step Process

1. Immediate Actions (Day 1)

- Ensure safety first

- Prevent further damage (tarp roof, board windows)

- Document everything with photos/videos

- Create list of damaged/destroyed items

2. Contact Your Insurer (Within 24-48 hours)

- Report the claim promptly

- Provide detailed account of what happened

- Get claim number and adjuster contact info

3. Meet with Adjuster

- Schedule convenient time

- Walk through damage together

- Provide documentation (receipts, photos, estimates)

- Don’t accept first offer if inadequate

4. Get Repair Estimates

- Obtain 2-3 independent estimates

- Use licensed, insured contractors

- Don’t start repairs until adjuster approves (except emergency mitigation)

5. Review Settlement Offer

- Compare with your estimates

- Question discrepancies

- Understand depreciation deductions

- Know you can negotiate

6. Complete Repairs

- Hire reputable contractors

- Keep all receipts

- Document completion

- Submit for final payment (if replacement cost coverage)

Typical Claim Timelines

| Claim Type | Average Settlement Time |

|---|---|

| Minor (under $5,000) | 7-14 days |

| Moderate ($5,000-$25,000) | 2-4 weeks |

| Major ($25,000-$100,000) | 4-8 weeks |

| Catastrophic (total loss) | 2-6 months |

| Disputed claims | 3-12+ months |

When to Consider a Public Adjuster

Hire a public adjuster if:

- Claim exceeds $20,000

- Insurer offers significantly less than your estimates

- You don’t have time to manage the process

- Claim is complex (fire, flood, extensive damage)

Cost: 10-15% of settlement (but can increase payout by 30-70%)

2026 Home Insurance Trends

Climate Change Impact

Severe weather events drive premium increases:

- Wildfire zones (West Coast): 15-35% increases

- Hurricane regions (Southeast): 20-50% increases

- Tornado Alley (Central US): 10-20% increases

- Flood-prone areas: 12-25% increases

Some insurers are withdrawing from high-risk states:

- State Farm, Allstate reducing California exposure

- Multiple insurers leaving Florida market

- Louisiana facing insurer insolvencies

Technology Integration

Smart Home Discounts Expanding Insurers partnering with smart home companies:

- Water leak detectors: 5-10% discount

- Smart thermostats: 2-5% discount

- Video doorbells: 3-7% discount

- Complete smart systems: Up to 20% discount

AI-Powered Claims Processing

- Photo-based estimates: Submit damage photos for instant assessment

- Drone inspections: Faster roof damage evaluation

- Virtual adjusters: Video chat claims processing

Usage-Based Insurance Similar to auto UBI, monitoring:

- Water usage patterns (leak detection)

- Electrical anomalies (fire prevention)

- HVAC efficiency (maintenance alerts)

Parametric Insurance

Emerging coverage type that pays predetermined amounts based on events:

- Hurricane makes landfall within X miles: Automatic $25,000 payout

- Earthquake magnitude exceeds X: Automatic $50,000 payout

- No adjuster needed, instant payment

Currently limited availability, expect expansion in 2026-2027.

Special Situations: Unique Coverage Needs

Home-Based Businesses

Standard policies provide minimal business property coverage ($2,500 typical limit):

- In-home business policy endorsement: $150-$400/year for $10,000-$25,000 coverage

- Business Owner’s Policy (BOP): For significant business operations

- Covers business equipment, liability, income loss

Short-Term Rentals (Airbnb, VRBO)

Standard policies don’t cover short-term rental activities:

- Proper coverage options:

- Dwelling fire policy with business liability

- Specialized short-term rental insurance

- Commercial property policy

- Cost: 25-50% more than standard homeowners

- Essential: Host liability coverage for guest injuries

Vacation/Second Homes

15-20% higher premiums due to:

- Extended vacancy periods

- Delayed damage discovery

- Higher vandalism/theft risk

Required coverage additions:

- Water damage endorsement

- Seasonal dwelling coverage adjustments

- Higher liability limits

Historic Homes

Challenges include:

- Irreplaceable materials and craftsmanship

- Higher rebuilding costs

- Code compliance issues

Solutions:

- Agreed value/guaranteed replacement cost policies

- Specialized historic home insurers

- Separate ordinance or law coverage

High-Value Homes

Homes valued over $750,000-$1,000,000 need:

- HO-5 or better coverage

- Higher liability limits ($500,000-$1,000,000 minimum)

- Umbrella policy for additional liability protection

- Scheduled valuables for jewelry, art, collectibles

Final Thoughts: Protecting Your Home in 2026

Home insurance is more than a mortgage requirement—it’s financial protection for your family’s future. While premiums continue rising, understanding what drives costs and implementing smart strategies can save you hundreds to thousands annually while maintaining comprehensive protection.

Key takeaways for 2026:

✓ Shop around every 2-3 years—rates vary dramatically between insurers ✓ Insure for replacement cost, not market value ✓ Bundle policies for 15-25% savings ✓ Invest in home protection (security, fire suppression) for discounts ✓ Raise deductibles if you have adequate emergency savings ✓ Document everything—inventory, receipts, photos ✓ Review coverage annually after renovations or major purchases ✓ Don’t file small claims—save insurance for major losses ✓ Consider additional coverage for floods, earthquakes, and valuables ✓ Understand your policy—know what’s covered and excluded

The 30-45 minutes spent comparing quotes and optimizing coverage can result in $500-$1,500 in annual savings while ensuring your home, belongings, and financial security remain protected.

Ready to save on home insurance? Start gathering quotes from multiple providers today, and don’t hesitate to work with an independent insurance agent who can help you navigate the complexities of homeowners insurance in your specific situation.