Finding affordable car insurance in 2026 feels like navigating a maze. With average premiums climbing to $2,150 annually for full coverage and over 50 insurance companies competing for your business, knowing how to compare quotes effectively can save you $500 to $1,200 per year. Whether you’re a first-time driver, a parent adding a teen to your policy, or simply looking to reduce your insurance costs, this comprehensive guide will show you how to find the cheapest auto insurance without sacrificing coverage.

Understanding Car Insurance Quotes in 2026

A car insurance quote is an estimate of how much you’ll pay for coverage based on your personal information, driving history, vehicle details, and coverage preferences. Unlike a simple price tag, auto insurance quotes are personalized to reflect your unique risk profile.

Insurance companies use sophisticated algorithms that analyze dozens of factors to calculate your premium. Understanding these factors puts you in control and helps you secure the best possible rates.

What Affects Your Car Insurance Quote?

Personal Factors

Age and Experience

- Drivers under 25 pay 60-100% more than drivers aged 30-50

- Senior drivers (65+) may see increases of 10-20%

- Teen drivers (16-19) face the highest premiums, often $3,000-$6,000 annually

Driving Record

- One at-fault accident: 20-40% increase

- DUI conviction: 80-150% increase for 3-5 years

- Speeding ticket: 15-25% increase

- Clean record for 3+ years: 10-25% discount

Credit Score In states where it’s permitted, credit-based insurance scores significantly impact rates:

- Excellent credit (750+): Baseline rates

- Good credit (700-749): 10-20% higher

- Fair credit (650-699): 25-40% higher

- Poor credit (below 650): 50-100% higher

Note: California, Hawaii, Massachusetts, and Michigan prohibit or limit credit-based insurance scoring.

Vehicle-Related Factors

| Vehicle Type | Average Annual Premium | Why It Costs More/Less |

|---|---|---|

| Sedan (Honda Accord) | $1,850 | Moderate repair costs, good safety ratings |

| SUV (Toyota RAV4) | $2,100 | Higher repair costs, better safety features |

| Luxury Car (BMW 5 Series) | $3,200 | Expensive parts, higher theft rates |

| Sports Car (Ford Mustang) | $2,900 | Performance capability, younger driver appeal |

| Electric (Tesla Model 3) | $2,600 | Expensive repairs, advanced technology |

| Pickup Truck (Ford F-150) | $2,050 | Durability, work vehicle perception |

Geographic Factors

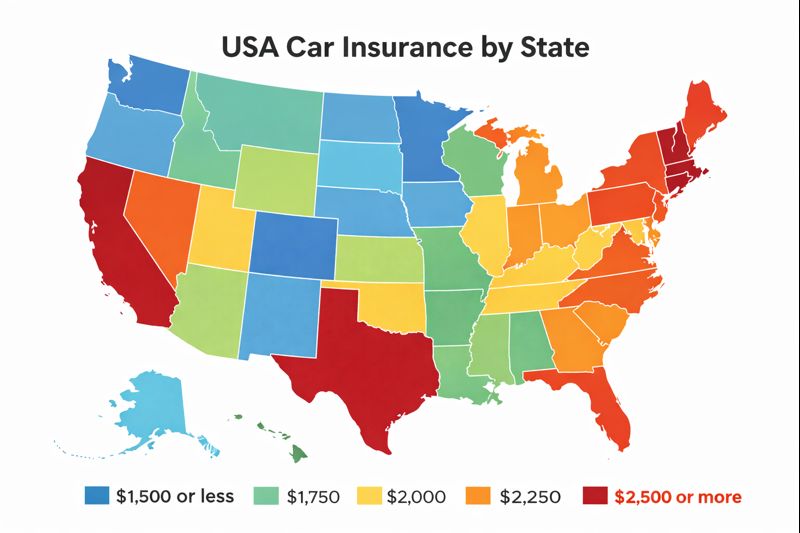

State Requirements Each state mandates different minimum coverage levels. In 2026, the most expensive states for car insurance are:

- Michigan: $3,785 average annual premium

- Louisiana: $3,450

- Florida: $3,200

- California: $2,650

- Nevada: $2,550

The cheapest states include:

- Maine: $1,150

- Vermont: $1,200

- Idaho: $1,250

- Iowa: $1,300

- Wisconsin: $1,350

Urban vs. Rural Urban drivers pay 25-50% more due to higher accident rates, theft, and vandalism. A driver in New York City might pay $3,500 while someone in rural upstate New York pays $1,800 for identical coverage.

Types of Car Insurance Coverage Explained

Required Coverage

1. Liability Insurance Covers damage and injuries you cause to others. This is mandatory in every state except New Hampshire and Virginia.

- Bodily Injury Liability: Pays medical expenses for injured parties

- Property Damage Liability: Covers damage to other vehicles and property

Typical coverage limits: 25/50/25 (minimum) to 250/500/100 (recommended)

2. Personal Injury Protection (PIP) / Medical Payments Required in no-fault states, covers medical expenses for you and passengers regardless of fault.

Optional but Recommended Coverage

3. Collision Coverage Pays for damage to your vehicle from accidents, regardless of fault. Average cost: $400-$800 annually.

4. Comprehensive Coverage Covers non-collision damage: theft, vandalism, weather, animal strikes. Average cost: $250-$450 annually.

5. Uninsured/Underinsured Motorist Coverage Protects you when hit by drivers with insufficient insurance. Highly recommended as 13% of U.S. drivers are uninsured.

6. Gap Insurance Covers the difference between your car’s value and loan amount. Essential if you:

- Financed more than 80% of the purchase price

- Have a loan longer than 60 months

- Drive a vehicle that depreciates quickly

Additional Coverage Options

- Rental Reimbursement: $20-40/year

- Roadside Assistance: $15-30/year

- Custom Parts Coverage: Varies by value

- Rideshare Coverage: $10-25/year (if you drive for Uber/Lyft)

Top Car Insurance Companies in 2026: Comparison

| Company | Average Annual Rate | Best For | Customer Satisfaction | Discount Opportunities |

|---|---|---|---|---|

| GEICO | $1,850 | Budget-conscious drivers | 4.3/5 | 15+ discounts available |

| State Farm | $2,100 | Local agent support | 4.5/5 | Loyalty, safe driving |

| Progressive | $1,950 | Online tools, customization | 4.2/5 | Name Your Price tool |

| USAA | $1,650 | Military members/families | 4.8/5 | Excellent military discounts |

| Allstate | $2,250 | Accident forgiveness | 4.1/5 | Safe driving bonuses |

| Liberty Mutual | $2,150 | Bundling options | 4.0/5 | Multiple policy discounts |

| Nationwide | $2,050 | Vanishing deductible | 4.3/5 | Accident-free rewards |

| Farmers | $2,200 | Customizable coverage | 4.2/5 | Good student, multi-car |

Best for Specific Situations

Cheapest Overall: GEICO and USAA consistently offer the lowest rates for most drivers.

Best for Young Drivers: State Farm and Nationwide offer competitive rates with good student discounts up to 25% off.

Best for Seniors: AARP members get excellent rates through The Hartford, with specialized coverage options.

Best for High-Risk Drivers: Progressive and The General specialize in non-standard insurance with SR-22 filing capabilities.

Best Mobile App: Progressive and Allstate lead with user-friendly apps and instant quote capabilities.

How to Compare Car Insurance Quotes Effectively

Step 1: Gather Your Information

Before requesting quotes, have this information ready:

- Personal details: Name, birthdate, address, marital status

- Driver’s license number and history

- Vehicle information: VIN, make, model, year, mileage

- Current insurance declarations page (if applicable)

- Driving history: Accidents and violations from past 3-5 years

Step 2: Determine Your Coverage Needs

Minimum vs. Recommended Coverage

While state minimums are cheaper, they often leave you financially vulnerable. Consider these recommendations:

- Liability: 100/300/100 minimum (many experts recommend 250/500/100)

- Deductibles: $500-$1,000 for comprehensive and collision

- Uninsured motorist: Match your liability limits

If your car is worth less than $3,000, consider dropping collision and comprehensive coverage.

Step 3: Use Multiple Quote Methods

Online Comparison Tools Websites like The Zebra, Insurify, and Policygenius let you compare multiple quotes simultaneously:

- Enter information once

- Receive 5-10+ quotes

- Filter by coverage, price, and company rating

- Time saved: 2-3 hours vs. individual company quotes

Direct Company Quotes Visit individual insurance company websites for potentially 5-10% lower rates than through comparison sites.

Independent Insurance Agents Work with agents who represent multiple companies:

- Personalized service

- Help navigating complex situations

- Access to regional carriers with competitive rates

- No cost to you (commissioned by insurers)

Step 4: Compare Apples to Apples

Ensure each quote includes:

- Identical coverage limits

- Same deductibles

- Equivalent optional coverages

- Similar discount applications

A quote that’s $200 cheaper might offer significantly less coverage, making it a poor value.

Maximum Discounts: How to Lower Your Car Insurance

Universal Discounts (Available from Most Insurers)

1. Multi-Policy/Bundle Discount: 15-25% savings Combine auto with home, renters, or life insurance.

2. Multi-Vehicle Discount: 10-20% savings Insure 2+ vehicles on the same policy.

3. Good Driver Discount: 15-30% savings Clean driving record for 3-5 years.

4. Defensive Driving Course: 5-15% savings Complete approved course (often required renewal every 3 years).

5. Paperless/Auto-Pay: 3-7% savings Opt for electronic documents and automatic payments.

6. Pay-in-Full: 5-10% savings Pay annual premium upfront instead of monthly installments.

Driver-Specific Discounts

Young Drivers

- Good student discount: 15-25% for B average or higher

- Distant student: 10-15% if attending school 100+ miles away without vehicle

- Driver training: 5-10% for completing approved courses

Experienced Drivers

- Mature driver: 5-10% for drivers 55+ who complete safety courses

- Low mileage: 10-20% for driving under 7,500 miles annually

- Retiree: 5-10% for retired drivers with reduced commute

Vehicle-Based Discounts

- Safety features: 5-15% for anti-lock brakes, airbags, anti-theft systems

- New vehicle: 5-10% for cars less than 3 years old

- Hybrid/electric: 5-10% from eco-friendly insurers

- Passive restraint: 10-20% for automatic seatbelts and airbags

Usage-Based Insurance (UBI) Programs

Telematics programs monitor your driving and reward safe habits:

- Progressive Snapshot: Save up to 30%

- State Farm Drive Safe & Save: Up to 30% savings

- Allstate Drivewise: Up to 40% savings

- GEICO DriveEasy: Up to 25% savings

These programs track:

- Hard braking frequency

- Acceleration patterns

- Time of day driving

- Miles driven

- Speed relative to limits

- Mobile phone use while driving

Average savings: 15-20% for safe drivers

Read Also: Commercial Property Insurance in the USA (2026): Cost, Coverage & Best Policies for Small Businesses

Common Mistakes When Shopping for Car Insurance

1. Focusing Only on Price

The cheapest quote isn’t always the best value. Consider:

- Company financial strength (AM Best rating of A- or higher)

- Customer service reputation

- Claims processing speed

- Coverage adequacy

A company that’s $15/month cheaper but takes 45 days to process claims may cost you more in the long run.

2. Not Shopping Around Regularly

54% of drivers haven’t compared rates in 3+ years, potentially overpaying $500-$800 annually. Insurance experts recommend comparing quotes:

- Annually at renewal

- After major life changes (marriage, move, new vehicle)

- When your policy increases without explanation

3. Accepting the First Renewal Quote

Many insurers raise rates at renewal, hoping you won’t notice. Call and negotiate or switch companies. Loyalty isn’t always rewarded—new customer discounts often beat loyalty discounts.

4. Overlooking Small Discounts

Small discounts stack up quickly:

- Bundle: 20%

- Good driver: 15%

- Multi-car: 15%

- Paperless: 5%

- Pay-in-full: 5% Total potential savings: 40-50% off base rates

5. Choosing Coverage Based on Vehicle Value Alone

Consider your financial situation, not just car value. If you can’t afford a $5,000 repair out-of-pocket, maintain collision coverage even on older vehicles.

Special Situations: Finding Insurance When It’s Difficult

High-Risk Drivers

If you have violations or accidents, consider:

- Progressive: Accident forgiveness program

- The General: Specializes in high-risk drivers

- State-assigned risk pools: Guaranteed coverage at higher rates

Tips for high-risk drivers:

- Take defensive driving courses

- Consider higher deductibles to lower premiums

- Ask about violation forgiveness programs

- Shop around—rate increases vary dramatically by company

First-Time Drivers

Without insurance history, you’ll pay premium rates:

- Get added to parent’s policy (if under 26): 50-70% cheaper than standalone

- Start with state minimum then increase coverage

- Ask about good student and driver training discounts

- Consider usage-based insurance to prove safe driving

Drivers with Gaps in Coverage

Gaps longer than 30 days can increase rates 5-15%. Minimize impact by:

- Explaining valid reasons (military deployment, living abroad, medical issues)

- Providing proof of alternative transportation

- Starting with the same insurer to maintain relationship

- Accepting higher rates temporarily while rebuilding history

2026 Car Insurance Trends You Should Know

Rising Premiums

Average premiums increased 8.4% in 2025 and are projected to rise another 6-7% in 2026 due to:

- Increased vehicle repair costs

- Supply chain issues for parts

- Rising medical costs

- More severe weather events

- Increased vehicle technology complexity

Technology Integration

More insurers offer:

- AI-powered claims processing: Settling simple claims in 24-48 hours

- Photo estimate apps: Submit damage photos for instant estimates

- Virtual inspections: No in-person appointments needed

- Blockchain verification: Faster multi-party claim resolution

Electric Vehicle Considerations

EV insurance costs 15-20% more on average due to:

- Expensive battery replacements ($5,000-$20,000)

- Specialized repair facilities

- Advanced technology repairs

- Higher vehicle values

However, some insurers offer EV-specific discounts offsetting these costs.

Climate Change Impact

Severe weather drives up claims in affected regions:

- Hurricane zones: 10-15% premium increases

- Wildfire areas: 8-12% increases

- Flood-prone regions: 6-10% increases

How to File and Maximize Your Claim

After an Accident

- Ensure safety and call police if needed

- Document everything: Photos, witness contacts, damage details

- Exchange information: Driver details, insurance, vehicle info

- Report promptly: Notify insurer within 24 hours

- Don’t admit fault: Let insurance companies determine liability

Working with Adjusters

- Get multiple repair estimates

- Understand depreciation vs. replacement cost

- Keep detailed records of all communications

- Don’t accept the first settlement if inadequate

- Consider hiring a public adjuster for large claims

Timeline Expectations

- Simple claims: 3-7 days

- Moderate claims: 2-4 weeks

- Complex claims: 4-8 weeks

- Disputed claims: 2-6 months

Final Thoughts: Getting the Best Car Insurance Quote in 2026

Finding the cheapest auto insurance requires effort, but the potential savings of $500-$1,200 annually make it worthwhile. Remember these key strategies:

✓ Compare at least 3-5 quotes from different companies ✓ Review coverage annually and after major life changes ✓ Maximize all available discounts—they stack significantly ✓ Balance price with coverage quality and company reputation ✓ Consider usage-based insurance if you’re a safe driver ✓ Don’t sacrifice essential coverage for minimal savings

The insurance landscape changes rapidly. What was cheapest last year may not be today. Dedicate 30-45 minutes annually to comparing quotes, and you’ll ensure you’re getting the best possible rates while maintaining adequate protection.

Ready to start saving? Use online comparison tools today, contact independent agents, and don’t be afraid to negotiate with your current insurer. Your wallet will thank you.